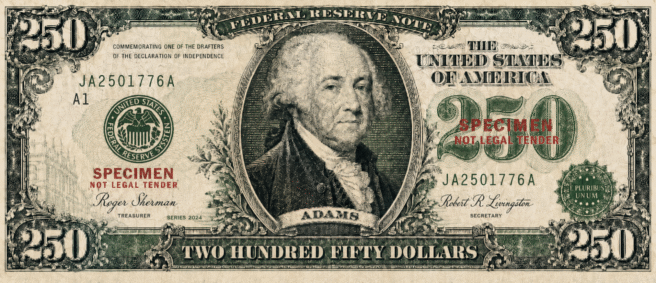

Friend-of-the-BLPB George Mocsary recently made me aware of his fun essay reproduced below. He also cleverly generated the related above image using ChatGPT, noting in sending it to me that “Roger Sherman and Robert R. Livingston, who are the fictitious Treasurer and Secretary signing the bill, were part of the Committee of Five who drafted the Declaration of Independence. The other three were John Adams (on this mock-up), Thomas Jefferson ($2 bill), and Ben Franklin ($100 bill).”

I love all of this. It is always interesting to see what business law profs think about and do outside the norm of their teaching, scholarship, and service. Enjoy George’s essay!

++++++++++++++++++++

A Modern Currency for a Modern Economy: Retiring the Single, Embracing the Coin, and Thinking Bigger

George A. Mocsary

Every day, Americans reach into their wallets and pull out a piece of currency that is fundamentally failing them and their nation: the one-dollar bill. We hold onto paper out of habit, resisting the mathematical realities of our monetary system. As we navigate a modern economy, the United States relies on an outdated physical currency structure. It is time for a comprehensive overhaul of our cash.

To bring our currency into the twenty-first century, the United States should execute a multi-step reform. First, we should stop printing the $1 bill. Second, we should replace it with the far more durable $1 coin. Third, we should elevate the $2 bill to serve as our standard low-denomination paper currency. Finally, we need to print bills significantly larger than the $100 note—the $500 bill or a novel $250 bill to celebrate the nation’s 250th anniversary. This is not just a matter of convenience. It is a matter of fiscal responsibility and international competitiveness.

The Cost of the Paper Single

The romanticism attached to the one-dollar bill is blinding us to its economic inefficiency. We currently treat our lowest paper denomination as a disposable commodity. According to the Federal Reserve, it costs approximately 4.1 cents to print a single $1 note. While that may sound inexpensive, the hidden cost lies in its shockingly short lifespan.

Due to the intense wear and tear of daily transactions, a $1 bill has an estimated lifespan of about seven years. The Federal Reserve must continuously order billions of new $1 notes each year to replace the ones that have been damaged, mutilated, or worn beyond recognition. This creates an expensive cycle of printing, distributing, evaluating, and shredding currency. The Bureau of Engraving and Printing operates at maximum capacity to keep up, wasting millions of taxpayer dollars on a product designed to fall apart in less than a decade.

A Durable Alternative: The $1 Coin

The solution to the paper single’s inefficiency is already in our pockets: the coin. It is time to fully replace the $1 bill with the $1 coin.

Although minting a modern dollar coin costs the U.S. Mint roughly 12 cents, focusing solely on the initial production cost is short-sighted. The true metric of currency efficiency is its lifespan. A $1 coin’s estimated lifespan is at least 30 years. In the time it takes a single dollar coin to wear out, the Federal Reserve would have had to print, distribute, and destroy roughly four distinct $1 bills. Aggregating these costs across the billions of singles in circulation, the math becomes undeniable. Independent analyses, including past reports from the Government Accountability Office (GAO), have repeatedly indicated that transitioning to a $1 coin and retiring the paper note would yield large financial benefits for the federal government once the higher production costs of $1 coins are recouped after about six years.

Bridging the Gap: The Rebirth of the $2 Bill

A common objection to the $1 bill’s elimination is that Americans still want a small-denomination paper note for tipping, minor purchases, and general convenience. Carrying pockets full of metal can be cumbersome. Fortunately, the Treasury already produces the perfect compromise: the $2 bill.

By stopping the production of the $1 bill, the government can easily scale up the printing of the $2 note. This fulfills the public’s desire for a low-denomination paper option while cutting the printing and pocket volume of small notes in half. The $2 bill is already legal tender, already familiar to the public, and ready to be deployed. Elevating it from a novelty item to a transactional staple would ensure a smooth, painless transition away from the $1 note.

The Missing Tier: Why We Need Larger Denominations

While our lower denominations suffer from inefficiency, our upper denominations suffer from a different problem: inflation-driven irrelevance. Since 1969, the United States has not issued a bill larger than the $100 note. But what was once a symbol of wealth is now barely enough to cover a standard trip to the grocery store or a family dinner out.

The rest of the world has long understood the value of large-denomination physical currency. Even as digital payments rise, the Eurozone maintains high-value physical notes, including the widely used €200 note (and the €500 note, which remains legal tender even though issuance has stopped). Switzerland seamlessly circulates the 1,000-franc note. This high-value piece of currency acts as a highly trusted store of wealth.

These nations issue such large notes because physical currency, in addition to serving as a medium of exchange, is a vital store of value. The U.S. dollar is the world’s reserve currency. Billions of U.S. dollars are held overseas by individuals and institutions who trust the stability of the American government more than their own local banking systems.

When a government issues high-denomination currency, it benefits from seigniorage. Seigniorage is the difference between the cost of producing currency and its face value. It is profit made by a government by issuing currency, especially when that currency is held indefinitely as a store of value rather than actively circulated. $100 bills currently boasts a lifespan of 24 years, largely because people hoard them rather than spending them daily. Providing even larger denominations would increase this longevity and seigniorage benefit, firmly cementing the U.S. dollar as the premier physical asset in the world.

A Bold Proposal: The $500 Bill or the Semiquincentennial $250 Note

To address this glaring gap at the top of our currency ladder, the United States should resume issuing a $500 bill. It should instantly become the premier physical store of value, reducing the bulk required to hold cash reserves and generating unprecedented seigniorage benefits for the federal government.

However, if a leap straight to $500 feels too drastic for policymakers, there is a uniquely American alternative: the introduction of a new $250 bill, rolled out as a test to coincide with the nation’s 250th anniversary in 2026.

At first glance, a $250 bill might seem unorthodox. We are accustomed to currency scaling in units of ones, fives, tens, and multiples thereof. Yet the $250 bill would be remarkably easy for the American public to adopt for one simple reason: the quarter.

Americans have used the 25-cent coin for generations. The cognitive math required to use a $250 bill is identical to the math required to use a quarter, just scaled up: two quarters equal fifty cents; two $250 bills equal $500. Four quarters equal a dollar; four $250 bills equal $1,000. Because the fractional logic is already hardwired into the American consumer’s brain, the learning curve for a $250 bill would be practically nonexistent. Moreover, introducing it as a commemorative but fully functional circulating note for the Semiquincentennial would generate substantial public interest, driving adoption and excitement.

Efficiency over Nostalgia

The United States’ currency is perhaps the nation’s most recognizable symbol. But nostalgia should not trump economic efficiency. Printing paper $1 bills that tear and degrade in a mere seven years is a drain of resources for which the 30-year $1 coin offers a vastly superior alternative. By embracing the coin, reviving the $2 bill for small paper transactions, and finally acknowledging the reality of modern economics by introducing a $250 or $500 note, the United States can fundamentally modernize its monetary system.

The nation is capable of making these pragmatic adjustments. In late 2025, the United States Mint ended production of the penny, closing a 232-year chapter in American coinage. The rationale was simple and undeniable: spending nearly four cents to manufacture a one-cent coin was an unjustifiable waste of taxpayer resources. The public adapted quickly to the reality of cash rounding, proving that nostalgia is a poor excuse for bad economics.

It is time for the United States Treasury and the Federal Reserve to think bigger and mint smarter. The mathematical evidence is clear, the international precedents are proven, and the opportunity presented by the Semiquincentennial provides the perfect moment to build a currency system that reflects the strength, durability, and scale of the modern American economy.