We’re at about two months since the last update on this front, and I wanted to share my current chart for 2025. As always, if you know about any moves that I’ve missed, please reach out.

I’ve got updated charts, differences of opinion about how well-developed Nevada’s case law is, some highlights and confusion about the Glass Lewis blog post on reincorporation that dropped today, and a quick highlight of the Guess, Inc. proxy that revealed its board had voted to attempt to move to Nevada before a take-private offer arrived.

Nevada

Nevada had another two public companies announce attempts to move to Nevada, Algorhythm Holdings and Capstone Holding.

| 2025 Nevada Domicile Shifts | |||

| Firm | Result | Notes | |

| 1. | Fidelity National Financial | Pass | |

| 2. | MSG Sports | Pass | |

| 3. | MSG Entertainment | Pass | |

| 4. | Jade Biosciences | Pass | Jade merged with Aerovate. |

| 5. | BAIYU Holdings | Pass | Action by Written Consent |

| 6. | Roblox | Pass | |

| 7. | Sphere Entertainment | Pass | |

| 8. | AMC Networks | Pass | |

| 9. | Universal Logistics Holdings, Inc. | Pass | Action by Written Consent |

| 10. | Revelation Biosciences | Fail | 97% of votes cast were for moving. There “were 1,089,301 broker non-votes regarding this proposal” |

| 11. | Eightco Holdings* | Fail | Votes were 608,460 in favor and 39,040 against with 763,342 broker non-votes. The proposal was filed in 2024 and the vote results were announced in 2025. It’s on the list for now, but you could also count it in 2024. |

| 12. | DropBox | Pass | Action by Written Consent |

| 13. | Forward Industries | Fail | This is New York to Nevada. Votes were 427,661 for and 96,862 against with 214,063 Broker Non-Votes. Proposal did not obtain majority of outstanding shares. |

| 14. | Nuburu | Fail | 87% of the votes cast were in favor of the proposal. 11% against 1.6% Abstained. There were 12,250,658 Broker Non-Votes. |

| 15. | Xoma Royalty | Pass | |

| 16. | Tempus AI | Pass | |

| 17. | Affirm | Pass | |

| 18. | Liberty Live | Pending | This is a split off from a Delaware entity to Nevada |

| 19. | Netcapital | Fail | This was a proposed move from Utah to Nevada. If failed with 541,055 votes in favor and 1,456,325 votes against. |

| 20. | Algorhythm Holdings | Pending | Meeting set for Nov. 20 |

| 21. | Capstone Holding Corp | Pending | Meeting set for Nov. 18 |

The Capstone Holding proxy contains this rationale for Nevada with an interesting bit bolded:

Nevada is a nationally-recognized leader in adopting and implementing comprehensive and flexible corporation laws that are frequently revised and updated to accommodate changing legal and business needs. In light of our growth, our Board believes that it will be beneficial to the Company and its stockholders to obtain the benefits of Nevada’s corporation laws. Nevada courts have developed considerable expertise in dealing with corporate legal issues and have produced a substantial body of case law construing Nevada corporation laws. Because the judicial system is based largely on legal precedents, the abundance of Nevada case law should serve to enhance the relative clarity and predictability of many areas of corporation law, and allow our Board and management to make business decisions and take corporate actions with greater assurance as to the validity and consequences of such decisions and actions.

This is not something I ordinarily hear about Nevada. My view is that our caselaw is somewhat limited, but that limitation is mitigated by our clear statute. Curious, I searched around on EDGAR and found a few other companies shifting to Nevada had used similar language in the past:

- Intelligent Buying in 2020. This was a proposal to go from California to Nevada.

- HFactor in 2023. This was a proposal to go from Georgia to Nevada.

- Oracle Health in 2022. This was a conversion from Delaware to Nevada.

Notably, this language contrasts with Fidelity National Financial‘s proxy which stated:

Nevada case law concerning the application of its statutes and regulations is more limited than in Delaware due in part to Nevada’s more statute-focused approach. As a result, to the extent Nevada’s statutes do not provide a definitive answer and a Nevada court must make a determination about issues concerning the Company’s governance without clear guidance or precedent, the Company and its stockholders may experience less predictability with respect to whether certain corporate decisions or transactions are proper and/or the extent to which stockholders maintain the right to challenge such decisions or transactions.

Texas

Texas recently picked up United States Antimony Corporation from Montana.

| 2025 Texas Domicile Shifts | |||

| Firm | Result | Notes | |

| 1. | Zion Oil and Gas | Pass | |

| 2. | Mercado Libre | Withdrawn | |

| 3. | Dillard’s | Pass | 12,791,756 votes for and 1,477,174 votes against |

| 4. | United States Antimony Corporation | Pass | Shift from Montana to Texas. 20,626,385 votes in favor. 11,816,235 against. 35,888,464 broker non-votes. |

Glass Lewis on Reincorporation

Earlier today, Glass Lewis released a blog post on reincorporation. I want to highlight a few findings and flag my concerns about the analysis on some points:

- Reincorporation attempts are on the rise. Glass Lewis evaluated 29 proposals in 2025, a 70.06% increase from 17 proposals in 2024 and a 45% increase above the 20 proposals in 2023.

- Controlled companies were much more likely to reincorporate. Glass Lewis found that 55% of the companies in their set had “significant or controlling shareholders”

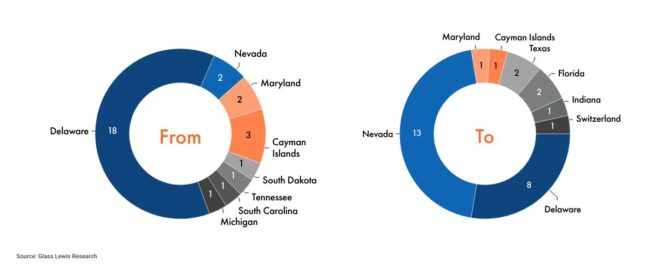

- Nevada surpassed Delaware as a reincorporation destination with 13 firms announcing for Nevada and 8 for Delaware.

- “Delaware companies have faced an increasingly litigious environment where shareholder lawsuits and the amount of plaintiff fees awarded have increased.”

All of these top-line findings make sene to me. I appreciate being able to see the Glass Lewis post as a way to cross-check my attempts to monitor this space. My largely hand-compiled set seems to have more firms than Glass Lewis. For example, Glass Lewis states:

While all but one reincorporation proposal from the 2025 proxy season was approved, average support for these proposals declined from 88.7% in 2024 to 81.1%. Revelation Biosciences was the only company that failed to receive majority support, with just 35% of the votes cast in favor and 60.9% abstaining. The overall decline in shareholder support indicates that shareholders were more critical of these proposals than in past seasons, particularly when the company proposed to leave Delaware.

This gave me pause for two reasons: (1) I don’t think that is correct factually; and (2) I have four other failed votes on my list, Eightco Holdings, Nuburu, Netcapital, and Forward Industries. Let’s run through my quibbles.

(1) The Math Seems Wrong

This is the Revelation Bioscience 8-K announcing results. Here is how it presents the vote information:

My calculation had 97% of the votes cast being in favor of the proposal. There were 2,956,575 votes in favor, 73,597 against, and 20,134 abstain. There were also 1,089,301 broker non-votes. Technically my math came out to 96.92716075% in favor. I’m not confident relying on the Glass Lewis post to conclude that shareholders are growing more critical of these proposals. It wasn’t just 35% of the votes cast that were in favor in Revelation Biosciences, it was about 97% of the votes cast being in favor. It didn’t pass because of the large number of broker non-votes.

(2) There Are Other Failed Votes

Here, I have five failed votes in 2025. It could be four total if you count Eightco in 2024. But I just don’t think it’s right.

- Eightco could go in 2024 or 2025 as the proposal came in December 2024 and the vote result came out in January 2025. I have it on my list, but it could just as easily be excluded.

- Nuburu held their meeting on July 9, 2025, and the results came out on July 14, 2025.

- Netcapital held its meeting on September 11, 2025, and the results came out on September 12, 2025.

- Forward Industries had results come out on August 12, 2025. Although it got a majority of votes cast, it did not win a majority of outstanding shares.

It may just be that I’m trying to catch anything that pops up on EDGAR and Glass Lewis is using a more limited set of companies on this one.

Other Concerns with Glass Lewis Post

But there are a few other things that jumped out at me as well: (1) Their charts seem to miss more reincorporation proposals; (2) the Nevada description isn’t quite right; and (3) it omits the Delaware Supreme Court opinion in Maffei.

(1) The Chart Omits Proposals

I haven’t tried to catch every reincorporation this year, so I don’t have a complete dataset here, but I think their chart on companies moving does not include all the 2025 action. Here, Glass Lewis has two companies attempting to go to Texas and I’ve got four. I also haven’t tried to track everything, just companies going to Nevada or Texas. This is the Glass Lewis chart:

It may be that Glass Lewis has their own internal definition for the 2025 Proxy Season and that their set is only capturing that information. It’s not explicit in the post, so that may explain the differences.

(2) Nevada Has Long Had A Specialized Business Court

I also want to drop a note about this line in the Glass Lewis post that could be read as indicating Nevada just now established a specialized business court.

Nevada’s amendments included: defining controlling shareholders and the fiduciary duties of controllers, establishing safe harbors in conflicted transactions, making certain adjustments to Nevada’s statutory business judgment rule, and establishing a specialized business court.

Here, I want to add a footnote that Nevada already has a specialized business court. It’s a business court docket handled by a subset of Nevada’s elected judges. The business court judges are currently selected by the Chief Judges in Clark and Washoe county from among the pool of elected judges. In the 2025 session, Nevada achieved first passage for a constitutional amendment to authorize the creation of an appointed business court. We also have a recently formed Judicial Commission to look at reorganizing and modernizing the existing business court.

(3) The Most Relevant Maffei Decision Came From Delaware’s Supreme Court

The Glass Lewis post states that:

recently the Delaware Court of Chancery and Delaware’s Supreme Court issued certain decisions on cases, specifically Maffei v. Palkon (TripAdvisor) and Tornetta v. Musk (Tesla), which were viewed as unfavorable toward controlling shareholders.

It is true that the Chancery decision in Maffei was not all that long ago. But the Glass Lewis post cites to a March 2024 Chancery opinion denying Maffei’s request for an interlocutory appeal. It does not mention that the underlying decision was reversed by the Delaware Supreme Court and that the controlling decision on the issue is now this February 2025 Delaware Supreme Court decision.

Guess, Inc.

Although I didn’t add it to the chart, Guess, Inc. also recently revealed that it had planned to propose a move to Nevada before a take-private offer arrived. On October 3, it put out a preliminary proxy statement with some interesting disclosures:

In August 2024, the Guess Board created a committee of the Guess Board comprised solely of independent and disinterested directors to evaluate a potential redomestication of Guess to a jurisdiction outside of Delaware (the “Redomestication Committee”). Willkie Farr and Gallagher LLP (“Willkie”) was retained by the Redomestication Committee as its legal counsel.

In November 2024, WHP approached Paul Marciano and Carlos Alberini regarding a potential strategic transaction involving Guess.. . .

In early February 2025, following months of deliberation, the Redomestication Committee of the Guess Board recommended, and the Guess Board resolved, that it was in the best interests of Guess and its stockholders for Guess to redomesticate to Nevada.

On March 13, 2025, the Guess Board received a letter from WHP. . . containing a non-binding proposal to acquire the outstanding shares of Guess Common Stock . . .

Following receipt of the WHP Proposal, the Redomestication Committee ceased consideration of a potential redomestication of Guess, and no such redomestication was ever effectuated.

What interests me about this is the timeline when companies consider whether they want to shift from one jurisdiction to another. It appears that Guess ran a seven-month process with an independent committee and counsel to evaluate the options. What we don’t know is the reasons the committee and board had for picking Nevada. Corporations often give different reasons in their proxy statements and it has been interesting to follow their rationales.