It’s the moment we’ve all been waiting for, and I am sorry to say – I was wrong.

(All right, in my heart, I still believe I was right in my account of existing law, and Salzberg v. Sciabacucchi actually changed the law. But, if law is just a prediction of what judges will do, then okay, fine, yes, I was wrong.)

As you all know by now, I’ve been blogging about this case, and the issue of litigation-limiting bylaw and charter provisions, for a while, and I’ve written an article, and a book chapter, on the subject. In this post, I’ll assume the reader’s familiarity with the issue and my prior argument.

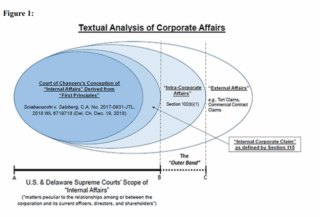

Anyway, the basic logic of the decision is illustrated by this figure from the opinion:

In other words, in the Delaware Supreme Court’s view, there are matters of internal affairs that are governed by the state of incorporation, and then there is a slightly larger category of matters that are still “intra-corporate” but not “internal affairs,” and can be governed by a corporation’s charter, and then there are truly external claims that cannot be the subject of a charter provision. Federal forum provisions for Section 11 claims, at least facially, count as intra-corporate claims because “FFPs involve a type of securities claim related to the management of litigation arising out of the Board’s disclosures to current and prospective stockholders in connection with an IPO or secondary offering. The drafting, reviewing, and filing of registration statements by a corporation and its directors is an important aspect of a corporation’s management of its business and affairs and of its relationship with its stockholders.” Op. at 11.

I’d love to do a full analysis of the decision but to be terribly honest, I’m just a wee bit distracted right now and also I found the opinion itself kind of … elliptical in its reasoning. Point being, I’ll give it a more thorough read at a later date but for now I’ve only got a series of quick points:

As I understand it, those matters that are sufficiently intracorporate to be the subject of a charter provisions, but not within the category of internal affairs, are to be determined case by case. But, per the Court’s earlier decision in ATP Tour, Inc. v. Deutscher Tennis Bund, 91 A.3d 554 (Del. 2014), even provisions related to antitrust lawsuits are at least facially permissible, so it’s going to be really interesting to find out what the court does, and does not, believe can be governed by corporate charters – and even more interesting to see if any other states (hello, California) push back. I’ll note that simply as a matter of terminology, I find the logic puzzling because the court quotes its own decision in McDermott v. Lewis, 531 A.2d 206 (Del. 1987), where the phrase “intracorporate” is treated as coextensive with “internal affairs.” Op. at 37. Moreover, apparently because the court couldn’t find better precedent, in explaining how external matters would be distinguished from intracorporate-but-not-internal-affairs matters, the court cited – well, Mohsen Manesh on the definition of the internal affairs doctrine. Op. at 47-48. Suffice to say, for those of us trying to figure out what falls into this middle category of “intracorporate” matters, a definition that distinguishes only between internal affairs and external affairs is not helpful.

As Larry Hamermesh says of the decision, “I thought we were in a predictable room, but the door has opened up into very uncertain challenges and positions.”

The case largely focuses on charter provisions, even going so far as to mention charter provisions specifically in its discussion of why forum selection clauses do not violate federal policy. Op. at 45. But occasionally, the decision cites to DGCL 109, regarding the bylaw power. I … do not know how to interpret this. And this is not a minor issue: Part of the reason I have been arguing that corporate constitutive documents cannot govern “external” claims is precisely because there’s no vocabulary outside the corporate law context to discuss whether a waiver, say, of a jury right, or an agreement to pay litigation expenses, should be in bylaws, charters, or both, or subject to supermajority voting provisions, or what happens if someone has dual-class stock or is a controller, etc. We know how to answer those questions when they concern matters of corporate law; we don’t when we step outside that realm.

The opinion very much hangs the NJAG out to dry. As I previously blogged here, here, and here, Professor Hal Scott has been pushing for bylaw at J&J which would mandate arbitration of all federal securities claims, including ones brought under Section 10(b)/10b-5. J&J is chartered in New Jersey. As part of the dispute over whether the proposal could be included on J&J’s proxy under Rule 14a-8, NJ’s Attorney General argued that such provisions violate NJ law, relying on Chancery’s Sciabacucchi decision. Now, that decision has been reversed. Professor Scott’s lawsuit will go forward and New Jersey will … I don’t know.

I think? there’s a basis for distinguishing Section 11 and 10b-5 in the opinion. The court emphasizes that Section 11 necessarily involves directors (“Section 11 claims are ‘internal’ in the sense that they arise from internal corporate conduct on the part of the Board and, therefore, fall within Section 102(b)(1)”), but 10b-5 does not. The court also says that tort claims are “external,” and 10b-5 is akin to common law fraud. But, umm … then there’s the antitrust thing so I really don’t know.

Further to this, the decision opens with a description of how both Section 11 and Section 12 claims operate. Section 12, like 10(b), also does not necessarily involve directors. But the opinion doesn’t discuss whether such claims count as intracorporate, even though the forum provisions at issue in the case cover both types of claims.

So, yeah. I got nothing.

I note that since the decision permits charters to govern securities claims, there is now apparently no barrier to inserting a loser-pays provision in corporate constitutive documents for federal securities claims. After all, the DGCL only bars loser-pays for internal claims. So, Professor Bainbridge’s preferred policy may yet (mostly) prevail. Which again highlights why I think this is a problem. If a corporation adopts such a provision, Delaware will have to decide if it’s permissible, if it violates public policy, whether the provision must be in the charter or the bylaws, what to do if there are nonvoting shares, etc, and that’s just way outside of its area of expertise. What happens when a director invokes a loser-pays provision and a shareholder argues that, under the circumstances, doing so was a breach of the director’s fiduciary duty? How will Delaware make the call? The Supreme Court has not, umm, demonstrated much savvy with respect to the difference between Section 11 and Section 12 claims (or, if you read some decisions, even the difference between a Schedule 14D-9 filing and a Schedule 14A), so I’m not confident of its ability make these judgments.

The Delaware Supreme Court should maybe start boning up on PSLRA pleading standards now, is what I’m saying.

Which brings us to arbitration. At the very end of the opinion, in Footnote 169, the court mentions that even though this case only involved forum selection provisions, many commenters – and I’d fall into this category, naturally – are concerned about using charters and bylaws to force individualized arbitration of shareholder claims. The court dismisses this concern on the grounds that DGCL 115 would prohibit mandatory arbitration for internal affairs claims. The problem here is twofold: First, the court opens the door to corporations adopting arbitration provisions for federal securities claims – precisely as Prof. Scott is currently arguing – but secondly, there looms the possibility that DGCL 115 is invalid under the Federal Arbitration Act.

Now, I wrote a whole long paper explaining why I believe the Federal Arbitration Act does not apply to corporate constitutive documents, but the basis for that article is that corporations are not ordinary contracts within the meaning of the FAA. Every decision – like this one – that expands the boundaries of the corporate “contract” and applies ordinary contract law principles to define its scope not only, ahem, renders my article less relevant, but also undermines the basis for excluding corporations from FAA’s purview. This is not an abstract issue; Professor Scott’s lawsuit, for example, argues that the FAA renders arbitration bylaws valid, regardless of any New Jersey law to the contrary. Again, his lawsuit only deals with a bylaw mandating arbitration of federal claims, but there is no reason the logic would not extend to bylaws purporting to mandate arbitration of internal affairs claims.

In other words, this decision hands corporations the keys to challenging the viability of DGCL 115, and in that respect, I have a sinking fear that it signs Delaware’s death warrant.

But people have made that prediction before, so who knows.

My final observation is this: I think the contrast between the Supreme Court and Chancery decisions as a matter of corporate theory are quite striking. The Chancery decision is a fairly stark example of the concession theory of the corporation: Laster makes very clear that Delaware, as sovereign, is intimately involved in establishing corporations, designing their operations, and articulating their limits. The Supreme Court, by contrast, is a model of contracts theory; it treats the corporation as simply a private arrangement among its constituents, with few prohibitions on what that arrangement may entail. I have been thinking about designing a corporate theory seminar; if it comes to fruition, I’ll likely include excerpts of both opinions.