Back when the SEC announced it was functionally no longer going to weigh in on whether companies may legally exclude shareholder proposals, I made a prediction in a number of spaces – except embarrassingly, I can’t remember which ones. Possibly podcasts, webinars, conferences, I’m sure someone remembers.

Which was: Companies now are in a heads-I-win, tails-you-lose position. They can exclude proposals, regardless of their legal basis for doing so. They can be confident that the SEC – which is now hostile to proposals – will not sue to force their inclusion. Very few shareholders will have the resources to sue over an improperly excluded proposal, and if any shareholder bothers, the company can simply moot the action by voluntarily agreeing to include the proposal even before filing an answer to a complaint. There is no risk to the company in simply excluding proposals, and waiting to see who sues.

And – behold!

AT&T said it would exclude a proposal offered by a variety of NYC pension funds asking for the company to disclose its EEOC-1, i.e., a form AT&T is required to submit to the federal government regarding the racial and gender makeup of its workforce. AT&T claimed that such a disclosure falls under the ordinary business exclusion of Rule 14a-8.

So, NYC pension funds – a well-heeled group of investors – filed a lawsuit, arguing that their proposal was not subject to the ordinary business exclusion. If you guessed it only took eight days for AT&T to agree to include the proposal on its proxy rather than litigate – you were correct.

A similar situation just unfolded with Pepsico; within days of the filing of a complaint, Pepsico agreed to include a proposal rather than litigate its exclusion.

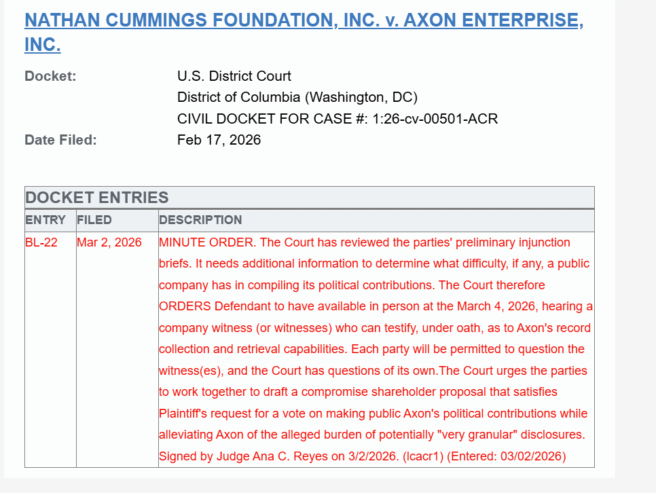

There remains, as far as I know, one other case along these lines; in that case, the defendant company, Axon, is litigating in response, but I suspect even if that goes on much longer, it will be an outlier. I suspect our future looks more like AT&T and Pepsico: wealthy investors will get their proposals included, either because companies voluntarily agree at the outset, or because they cave at the filing of a complaint; investors without those resources will be excluded. And note, this is not about the actual size of the investor’s stake; plenty of investors may have small stakes but resources to litigate, and that’s what will carry the day. If anything, this will make the proposal process more political, rather than less, because interest groups are more likely to have litigation infrastructure.

And another thing. In this week’s Shareholder Primacy podcast, Mike Levin and I talk about efforts to regulate proxy advisors at the state level. Here at Apple; here at Spotify; and here at YouTube.

Update:

Update 2:

Axon settles. The point is not to litigate this stuff.