I’m too busy to blog today because I am preparing a training presentation on governance duties for nonprofits. The audience will consist of high level staff, not board members. I have served on many nonprofits and have advised others but I would be interested in your thoughts. Do you teach nonprofit law? Do you sit on nonprofits? What issues do you think nonprofit board members and staffer should know? Among other things, I plan to focus on fiduciary duties, maintaining 501(c)(3) exemption status, agency issues, the implications of Sarbanes-Oxley, conflicts of interest, document retention, code of ethics/whistleblower (to comport with 990),why nonprofits get sued, compensation issues, lobbying, insurance and indemnification, the role of different committees (particularly the audit committee), how to take good minutes, etc. I plan to use hypotheticals to help make the points stick. If you can think of other matters for my 3 hour module or some good case studies, please comment below or inbox me at mnarine@stu.edu.

Corporate Governance

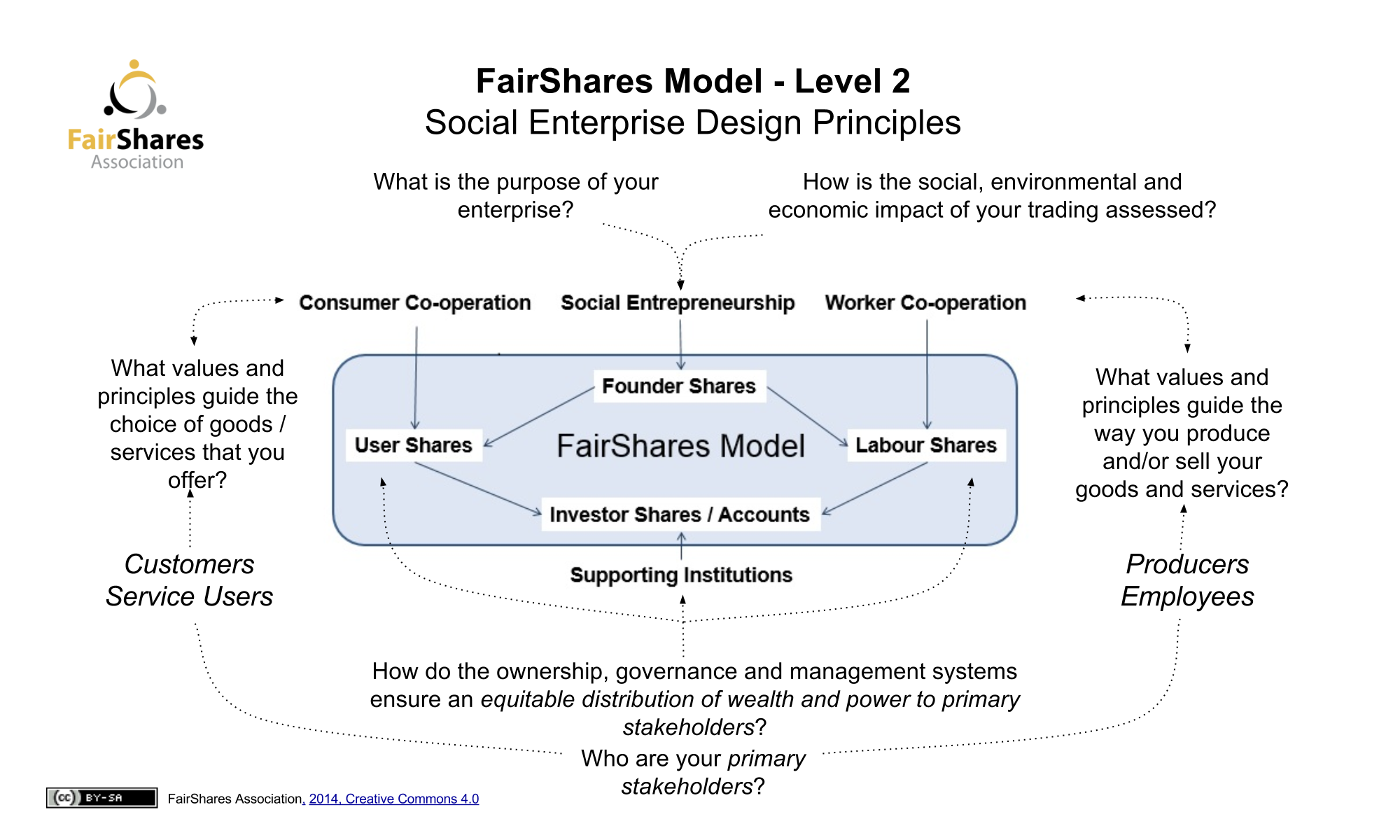

The FairShares Model

By Joan Heminway on

On of the many interesting things discussed during the social enterprise law workshop at Notre Dame Law School was the “FairShares Model.” Nina Boeger (University of Bristol-UK) brought the model to the group’s attention, and the model was new news to me.

The FairShares Model was “created during a research programme on democratising charities, co-operatives and social enterprises involving academics at Sheffield Hallam University and Manchester Metropolitan University in the UK.”

The FairShares Model cites the “Social Enterprise Europe Ltd” when noting that social enterprises “aim to generate sustainable sources of income, but measure their success through:

-

Specifying their purpose(s) and evaluating the impact(s) of their trading activities;

-

Conducting ethical reviews of their product/service choices and production/consumption practices;

- Promoting socialized and democratic ownership, governance and management.”

To address theses aims, the FairShares Model offers social audits and suggests the issuing some combination of (1) founder shares, (2) labour shares, (3) investor shares, (4) user shares.

{kind=link}

While I agree that significant corporate governance changes should be considered, at first glance this model seems a bit unwieldy if all four types of shares are issued. Still, I am interested in learning more.

Adopting Stakeholder Advisory Boards Article is Posted

By Joan Heminway on

With co-editor Joan Heminway (and Anne Tucker via Skype), I am at Notre Dame for a symposium on social enterprise law. I will be presenting on aforthcoming book chapter, which builds on my stakeholder advisory board idea. My article Adopting Stakeholder Advisory Boards article was recently published in the American Business Law Journal and I posted it to SSRN this week. The abstract is reproduced below.

———–

Over the past decade, interest in socially responsible business has grown exponentially. The social business movement seeks to have firms focus on the interests of all corporate stakeholders, rather than solely the financial interests of shareholders. Coupled with the social business movement of the past decade has been the passage of social enterprise statutes by over thirty states. The social enterprise statutes provide legal frameworks for firms that seek profit alongside broader social and environmental ends. A plethora of social enterprise legal forms have been created in the United States since 2008, including benefit corporations, public benefit corporations, benefit LLCs, low-profit limited liability companies (L3Cs), general benefit corporations, specific benefit corporations, sustainable business corporations, and social purpose corporations.

Despite the interest in social business and the passage of numerous social enterprise laws, the basic…

Conference on Doing Business in Cuba: Legal, Ethical, and Compliance Challenges

By Marcia Narine Weldon on

Businesses from small farmers to cruise lines are anxiously awaiting President Trump’s policy on Cuba and how/if he will rescind President Obama’s Executive Orders relaxing restrictions on doing business with the island.

If you’re in the South Florida area next Friday March 10th, please consider attending the timely conference on Doing Business in Cuba: Legal, Ethical, and Compliance Challenges from 8:00 am-4:30 pm at the Andreas School of Business, Barry University. The Florida Bar has granted 6.5 CLE credits, including for ethics and for certifications in Business Litigation and International Law. The Miami-Dade Commission on Ethics and Public Trust is organizing the event.

As a member of the Commission and an academic who has just completed my third article on Cuba, I’m excited to provide the opening address for the event. I’m even more excited about our speakers John Kavulich, President, U.S. Cuba Trade and Economic Council Inc; the general counsel of Carnival Cruise Lines; mayors of Miami Beach, Coral Gables, and Doral; director of the Miami International Airport; a number of academic experts from local universities; Commissioners Nelson Bellido and Judge Lawrence Schwartz; and outside counsel from MDO Partners, Akerman LLP, Holland & Knight, Greenberg Traurig, Squire Patton Boggs…

Bruner on “Center-Left Politics and Corporate Governance: What Is the ‘Progressive’ Agenda?”

By Colleen Baker on

Christopher Bruner has posted Center-Left Politics and Corporate Governance: What Is the ‘Progressive’ Agenda? on SSRN. You can download the paper here. Here is the abstract:

For as long as corporations have existed, debates have persisted among scholars, judges, and policymakers regarding how best to describe their form and function as a positive matter, and how best to organize relations among their various stakeholders as a normative matter. This is hardly surprising given the economic and political stakes involved with control over vast and growing “corporate” resources, and it has become commonplace to speak of various approaches to corporate law in decidedly political terms. In particular, on the fundamental normative issue of the aims to which corporate decision-making ought to be directed, shareholder-centric conceptions of the corporation have long been described as politically right-leaning while stakeholder-oriented conceptions have conversely been described as politically left-leaning. When the frame of reference for this normative debate shifts away from state corporate law, however, a curious reversal occurs. Notably, when the debate shifts to federal political and judicial contexts, one often finds actors associated with the political left championing expansion of shareholders’ corporate governance powers, and those associated with the political right advancing…

The President and Responsible Business Conduct

By Marcia Narine Weldon on

This post does not concern President Trump’s own business empire. Rather, this post will be the first of a few to look at how the President retains, repeals, or replaces some of the work that President Obama put in place in December 2016 as part of the National Action Plan on Responsible Business Conduct. Many EU nations established their NAPS year ago, but the U.S. government engaged in two years of stakeholder consultations and coordinated with several federal agencies before releasing its NAP.

Secretary of State Tillerson will play a large role in enforcing or revising many of the provisions of the NAP because the State Department promotes the Plan on its page addressing corporate social responsibility. Unlike many federal government pages, this page has not changed (yet) with the new administration. As the State Department explained in December, “the NAP reflects the government’s commitment to promoting human rights and fighting corruption through partnerships with domestic and international stakeholders. An important part of this commitment includes encouraging companies to embrace high standards for responsible business conduct.” Over a dozen federal agencies worked to develop the NAP.

We now have a new Treasury Secretary and will soon have a…

First Standalone Publicly Traded Benefit Corporation – Laureate Education

By Joan Heminway on

Laureate Education recently became the first standalone publicly traded benefit corporation. They are organized under Delaware’s public benefit corporation (PBC) law, are also a certified B corporation, and will be trading as LAUR on NASDAQ.

Plum Organics, also a Delaware PBC, is a wholly owned subsidiary of publicly-traded Campbell Soup Company. And Etsy is a publicly traded certified-B corporation, but is organized under traditional Delaware corporation law.

Whether the for-profit educator Laureate will hurt or help the popularity of benefit corporations remains to be seen, but some for-profit educators have not been getting good press lately.

Inside Higher Ed reports on Laureate Education’s IPO as a benefit corporation below:

The largest U.S.-based for-profit college chain became the first benefit corporation to go public Wednesday morning.

Laureate Education, which has more than a million students at 71 institutions across 25 countries, had been privately traded since 2007. Several major for-profit higher education companies have over the last decade bounced back and forth between publicly and privately held status; also yesterday, by coincidence, the Apollo Group, owner of the University of Phoenix, formally went back into private hands….In its public debut, the company raised $490 million….

Becker

…

What do we know about the future of corporate governance and compliance so far under Trump?

By Marcia Narine Weldon on

Shortly after the election in November, I blogged about Eleven Corporate Governance and Compliance Questions for the President-Elect. Those questions (in italics) and my updates are below:

- What will happen to Dodd-Frank? There are already a number of house bills pending to repeal parts of Dodd-Frank, but will President Trump actually try to repeal all of it, particularly the Dodd-Frank whistleblower rule? How would that look optically? Former SEC Commissioner Paul Atkins, a prominent critic of Dodd-Frank and the whistleblower program in particular, is part of Trump’s transition team on economic issues, so perhaps a revision, at a minimum, may not be out of the question.

Last week, via Executive Order, President Trump made it clear (without naming the law) that portions of Dodd-Frank are on the chopping block and asked for a 120-day review. Prior to signing the order, the President explained, “We expect to be cutting a lot out of Dodd-Frank…I have so many people, friends of mine, with nice businesses, they can’t borrow money, because the banks just won’t let them borrow because of the rules and regulations and Dodd-Frank.” An executive order cannot repeal Dodd-Frank, however. That would require a vote of 60…

Appraisal Standard Intellectual “Cage Match”: DFC Global Corp Amici Briefs

By Anne Tucker on

Prominent corporate governance, corporate finance and economics professors face off in opposing amici briefs filed in DFC Global Corp. v. Muirfield Value Partners LP, appeal pending before the Delaware Supreme Court. The Chancery Daily newsletter, described it, in perhaps my favorite phrasing of legal language ever: “By WWE standards it may be a cage match of flyweight proportions, but by Delaware corporate law standards, a can of cerebral whoopass is now deemed open.”

Point #1: Master Class in Persuasive Legal Writing: Framing the Issue

Reversal Framing: “This appeal raises the question whether, in appraisal litigation challenging the acquisition price of a company, the Court of Chancery should defer to the transaction price when it was reached as a result of an arm’s-length auction process.”

vs.

Affirmance Framing: “This appeal raises the question whether, in a judicial appraisal determining the fair value of dissenting stock, the Court of Chancery must automatically award the merger price where the transaction appeared to involve an arm’s length buyer in a public sale.”

Point #2: Summary of Brief Supporting Fair Market Valuation: Why the Court of Chancery should defer to the deal price in an arm’s length auction

- It would reduce litigation and

…

Executives and the Executive Order

By Marcia Narine Weldon on

Donald Trump has had a busy two weeks. Even before his first official day on the job, then President-elect Trump assembled an economic advisory board. On Monday, January 23rd, President Trump held the first of his quarterly meetings with a number of CEOs to discuss economic policy. On January 27th, the President issued what some colloquially call a “Muslim ban” via Executive Order, and within days, people took to the streets in protest both here and abroad.

These protests employed the use of hashtag activism, which draws awareness to social causes via Twitter and other social media avenues. The first “campaign,” labeled #deleteuber, shamed the company because people believed (1) that the ride-sharing app took advantage of a work stoppage by protesting drivers at JFK airport, and (2) because they believed the CEO had not adequately condemned the Executive Order. Uber competitor Lyft responded via Twitter and through an email to users that it would donate $1 million to the ACLU over four years to “defend our Constitution.” Uber, which is battling its drivers in courts around the country, then established a $3 million fund for drivers affected by the Executive Order. An…