(Previously.) Here is one company’s method for avoiding inclusion:

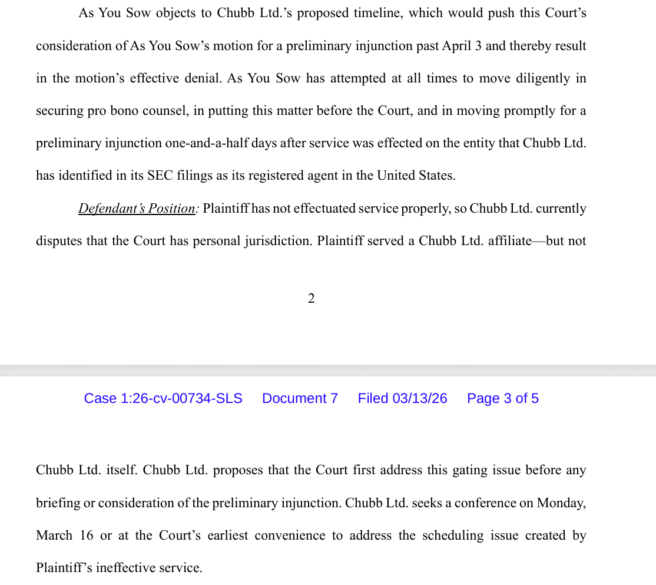

Service. They’re contesting service.

(Previously.) Here is one company’s method for avoiding inclusion:

Service. They’re contesting service.

I’ve previously blogged a couple of times about SPVs as a vehicle for investing in private companies. They not only skirt the law regarding the number of investors a company can have before it is required to make public disclosures, but they also may layer on high fees and suspect valuations – and that’s if they aren’t outright fraudulent.

Anyway, I post because Bloomberg had a nice feature on this yesterday, pointing out both the risk of fraud, and simply the risk of losing one’s shirt. (It references two lawsuits that have been filed in Delaware over these vehicles; if I’m right, one I blogged about before, and the other is this one, where a fund put $10 million into an SPV that was supposed to acquire SpaceX shares, and doesn’t seem to be able to get any financial reports.)

But even aside from actual fraud cases, the SPV may only have shares in another SPV that somewhere down the line has shares, and leaving aside valuation and fee questions, when the company does go public, those shares might be locked up and nontradeable for some period of time, leaving the SPVs holding illiquid investments that could

ExxonMobil is a Texas corporation in all but name, with most senior corporate executives and all corporate functions based in the state for the last 35 years. Our global headquarters are

Sorry, Ben, I’m jumping on this one.

Exxon is proposing to move its domicile to Texas.

It’s an obvious move for Exxon; their headquarters are there so they’re not exposing themselves to lawsuits in a different venue, and they also perhaps expect, shall we say, a friendlier judicial reception in Texas.

But Exxon isn’t a Delaware company. It’s a New Jersey one, old school from when it was Standard Oil and New Jersey dominated the market for corporate charters. Right now, they’re the subject of a couple of lawsuits in New Jersey over their retail shareholding program, and they’re fighting to transfer those to Texas.

But Exxon doesn’t have a controlling shareholder; its shareholders are normie institutions like BlackRock and State Street.

Perhaps to placate them over the move, it’s explicitly not going to opt in to the Texas provisions that would allow ownership thresholds on shareholder proposals and derivative lawsuits – provisions that did not exist when, say, Tesla asked them to vote on a move.

But, it’s also not committing in the charter not to adopt those provisions in a unilateral director-passed bylaw in the future (compare, for example, ArcBest, which promised in the charter

I begin with illegality. Under Delaware law, contracts “purport[ing] to require a board to act or not act in such a fashion as to limit the exercise of fiduciary duties” are “invalid and unenforceable.” In the merger context, a board may not “disable[] itself from exercising its own fiduciary obligations at a time when the board’s own judgment is most important, i.e., receipt of a subsequent superior offer.” For example, “[d]irectors cannot be precluded by the terms of an overly restrictive ‘no-shop’ provision from all consideration of possible better transactions.”64 Boards are required to bargain for effective fiduciary out clauses permitting them to discharge their managerial authority in fidelity to stockholders. When managerial authority is preserved, the Court will

Following up on January’s post on this topic, we have some updates. This is the list I’ve compiled so far.

Announced Moves as of February 26

| Company Name | Stock Ticker | Origination State | Destination State |

| TruGolf | TRUG | Delaware | Nevada |

| Forian, Inc. | FORA | Delaware | Maryland |

| LQR House | YHC | Nevada | Delaware |

| CBAK Energy | CBAT | Nevada | Cayman Islands |

| Cheetah Net | CTNT | North Carolina | Delaware |

| Galecto | GLTO | Delaware | Cayman Islands |

| Resolute Holdings Management, Inc. | RHLD | Delaware | Nevada |

| Forward Industries, INC | FWDI | New York | Texas |

| EQV Ventures Acquisition | FTW | Cayman Islands | Delaware |

| Datadog, Inc. | DDOG | Delaware | Nevada |

| Haymaker Acquisition Corp 4 | HYAC | Cayman Islands | Delaware |

| CDT Equity | CDT | Delaware | Cayman Islands |

| eXp World Holdings | EXPI | Delaware | Texas |

| ArcBest Corp | ARCB | Delaware | Texas |

We’ve got an additional seven entries since the last update with some multi-billion dollar companies announcing for Texas now, including ArcBest which came out today.

To make this easier to understand, I’ve recruited a couple of Research Assistants to help with data visualizations, so many thanks to Ethan Viator and Hunter Hawkins for helping pull these together. You can see my full data here with some notes for follow up from our two brave research assistants. I’ve also added a column to track disclosed

Back when the SEC announced it was functionally no longer going to weigh in on whether companies may legally exclude shareholder proposals, I made a prediction in a number of spaces – except embarrassingly, I can’t remember which ones. Possibly podcasts, webinars, conferences, I’m sure someone remembers.

Which was: Companies now are in a heads-I-win, tails-you-lose position. They can exclude proposals, regardless of their legal basis for doing so. They can be confident that the SEC – which is now hostile to proposals – will not sue to force their inclusion. Very few shareholders will have the resources to sue over an improperly excluded proposal, and if any shareholder bothers, the company can simply moot the action by voluntarily agreeing to include the proposal even before filing an answer to a complaint. There is no risk to the company in simply excluding proposals, and waiting to see who sues.

And – behold!

AT&T said it would exclude a proposal offered by a variety of NYC pension funds asking for the company to disclose its EEOC-1, i.e., a form AT&T is required to submit to the federal government regarding the racial and gender makeup of its workforce. AT&T claimed

I read with interest this FBI Most Wanted notice concerning a certain Joshua Link, who is accused of, well:

Joshua Robert Link is wanted for his alleged involvement in a fraud scheme between January of 2021 and December of 2023. Through his company, Agridime LLC, Link and his co-conspirators solicited cattle contracts from buyers throughout the United States. They told prospective buyers that Agridime would purchase cattle, care for and feed the cattle, have it processed, and sell the meat through Agridime’s distribution channels. Agridime offered investment returns from 15% to 32% to prospective cattle contract buyers. In reality, Agridime purchased only a fraction of the cattle. The scheme resulted in an approximate loss of $115 million to over 2,000 cattle contract buyers nationwide. On January 29, 2026, a federal arrest warrant was issued for Link in the United States District Court, Northern District of Texas, Fort Worth Division, after he was charged with Conspiracy to Commit Wire Fraud.

Upon further research, I discovered that the SEC had previously brought a civil action against him and his co-conspirators. As I understand the scheme, the fraudsters sold specific cattle to individual investors, promised to hold on to the cattle, raise, feed

The Weinberg Center has launched a short, anonymous survey of law professors on normative views of the shareholder proposal system under Rule 14a-8. The survey may take about 10–12 minutes. A link to the survey is available here:

https://www.surveymonkey.com/r/YWPHSC2

If you have any questions about the survey, you can reach out to Larry Cunningham.

It was reported this week that OpenAI has disbanded its mission alignment team, and fired a woman (ostensibly because she discriminated against men) who opposed adding an “Adult Mode” to ChatGPT. Meanwhile, a former OpenAI researcher published a NYT op-ed about the erosion of OpenAI’s principles.

Notably, these moves come after OpenAI’s contentious restructuring into a Delaware public benefit corporation, which required assurances to the AGs of California and Delaware that the new structure would remain true to OpenAI’s original nonprofit mission to develop AI for humanity’s benefit. The way this was supposed to occur was that OpenAI-the-nonprofit was given a golden share to control OpenAI-the-benefit-corporation’s board.

The available evidence suggests … the mission may have been redirected.

Now, maybe that’s because of the identity of the individuals appointed to OpenAI-the-nonprofit’s board, which include current and former tech execs, a private equity guy, a corporate lawyer, and Sam Altman. And certainly, there may be a broader lesson here about the general toothlessness of the benefit corporation form – we’re seeing similar issues at Anthropic, which is also organized as a benefit corporation.

But the problem likely runs deeper. For one thing, we all remember