On of the many interesting things discussed during the social enterprise law workshop at Notre Dame Law School was the “FairShares Model.” Nina Boeger (University of Bristol-UK) brought the model to the group’s attention, and the model was new news to me.

The FairShares Model was “created during a research programme on democratising charities, co-operatives and social enterprises involving academics at Sheffield Hallam University and Manchester Metropolitan University in the UK.”

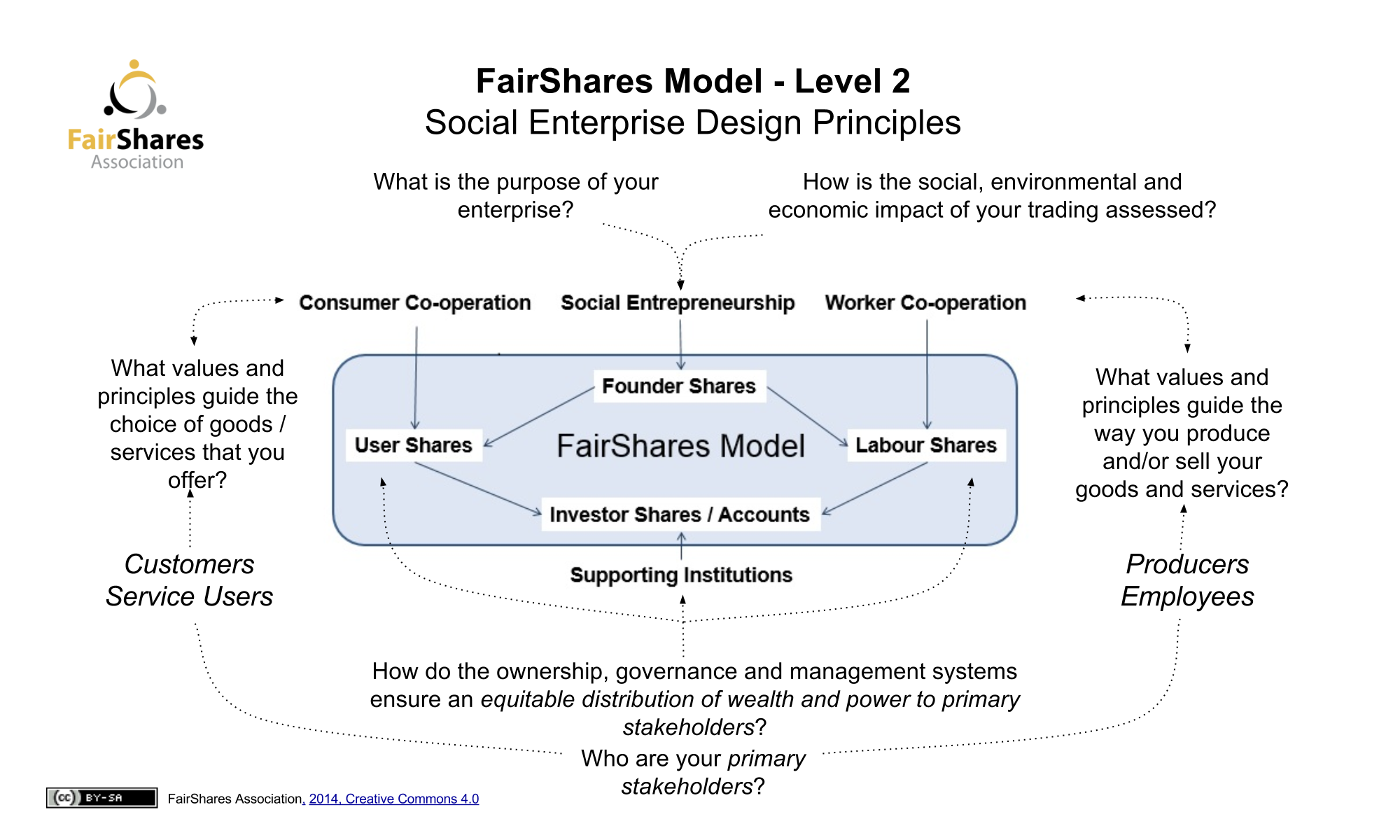

The FairShares Model cites the “Social Enterprise Europe Ltd” when noting that social enterprises “aim to generate sustainable sources of income, but measure their success through:

-

Specifying their purpose(s) and evaluating the impact(s) of their trading activities;

-

Conducting ethical reviews of their product/service choices and production/consumption practices;

- Promoting socialized and democratic ownership, governance and management.”

To address theses aims, the FairShares Model offers social audits and suggests the issuing some combination of (1) founder shares, (2) labour shares, (3) investor shares, (4) user shares.

{kind=link}

While I agree that significant corporate governance changes should be considered, at first glance this model seems a bit unwieldy if all four types of shares are issued. Still, I am interested in learning more.